When Local Law Meets Global Complexity

What the French e-invoicing reform is revealing about how large international groups are — and aren’t — organized to handle regulatory change.

The deadline is real. The penalties are real. And yet, across boardrooms and finance functions of major international groups, the same slow-motion crisis keeps unfolding: a local regulatory mandate lands, and the organization discovers — too late — that it is simply not built to respond at the speed the law requires.

France’s e-invoicing reform is the latest stress test. But the dysfunction it exposes is not new. For any large multinational headquartered outside Europe — particularly US-based groups operating across dozens of legal entities on multiple continents — a local compliance obligation in a single country can trigger a chain reaction of organizational failures that no one fully anticipated. At Coffra group, working directly through this transformation and supporting multinationals navigating it, we are watching these patterns emerge in real time. What follows is not theory. It is what we are learning on the ground.

The Complexity No One Budgeted For

When a country like France mandates electronic invoicing — with specific format requirements, certified platform obligations, clearance models, and strict timelines — the assumption at the group level is often:

“This is a local IT issue. Let the subsidiary handle it.”

That assumption is dangerous.

The French reform doesn’t just affect how invoices are sent. It touches master data quality, enterprise resource planning configurations, intercompany flows, tax reporting logic, and the way entities interact with customers and suppliers. For a US-headquartered group with French operations embedded inside a global enterprise resource planning template, every one of those layers requires a cross-functional decision — often involving people in three time zones who have never worked together before.

The complexity is not just technical. It is organizational. And most large groups are not structured to absorb it quickly.

Four Pitfalls We See Repeatedly

- Timeline shock — discovering the deadline too late

Regulatory timelines in France are communicated in French, through French official channels, often updated with short notice. By the time an obligation surfaces on the radar of a group tax or compliance function in the US, months have already been lost. What looked like an 18-month runway has quietly become a 6-month emergency. Decisions that should have been strategic are now reactive — and expensive.

- No single owner — tax, IT, and finance point at each other

E-invoicing sits at the intersection of tax law, finance operations, and IT infrastructure. In most large groups, no single function owns all three. Tax says it’s an IT project. IT says it needs a business owner. Finance says it’s waiting for specs from tax. In the meantime, nothing moves. We see this governance vacuum consistently — and it is the single biggest cause of project delays.

- Subsidiaries dragging their feet — or going rogue (independent)

Local entities are busy. They have their own priorities, their own reporting lines, and often a healthy skepticism toward mandates that arrive from group level with little context. Some delay responses. Others launch their own solutions — selecting local vendors, reconfiguring systems — without group alignment. Both behaviors are rational from a local perspective. Both are catastrophic from a group one.

- Data and enterprise resource planning fragmentation across entities

E-invoicing mandates require clean, structured, consistent data: tax registration numbers, VAT codes, address formats, and value mapping to local invoicing formats. In groups that have grown through acquisition, this data is rarely clean, rarely consistent, and rarely governed. The compliance project forces a data quality reckoning that no one planned for — adding weeks or months to timelines that were already tight.

What Effective Coordination Actually Looks Like

The multinationals that navigate these reforms successfully are not necessarily the largest or the best-resourced. They are the ones that treat local regulatory compliance as a group-level program — not a local IT ticket.

Concretely, that means three things:

- Establish a global steering structure with local accountability. One executive sponsor at group level. One named lead per impacted entity. A governance rhythm that is regular, documented, and binding. This sounds basic. It is consistently absent.

- Create a single source of truth for regulatory intelligence. Don’t rely on subsidiaries to surface obligations upward. Invest in proactive regulatory monitoring, mapped to your entity footprint. Know what is coming before it arrives — in every jurisdiction where you operate.

The Bigger Picture: France Is Not the Exception

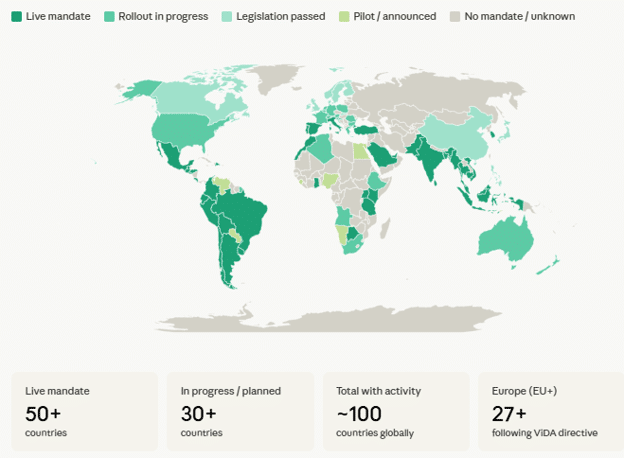

France’s e-invoicing reform is one of more than 80 active or upcoming e-invoicing and e-reporting mandates worldwide. Italy, Spain, Germany, Poland, Saudi Arabia, India, Brazil — the wave is global, accelerating, and arriving at different speeds in different markets. For a multinational managing 20, 30, or 50 legal entities, the question is no longer whether a local mandate will create group-level complexity. It is whether your organization is built to absorb that complexity — repeatedly, simultaneously, across jurisdictions.

Most are not. Yet.

Are You Ready?

If your group is currently navigating the French reform — or anticipating the next wave of mandates — ask yourself honestly:

- Do you have a named owner who sits across tax, IT, and finance?

- Do you have visibility into your subsidiary readiness right now — not in 60 days?

- Is your data clean enough to meet format requirements on day one?

- Do you have a regulatory monitoring function, or are you waiting for subsidiaries to tell you what’s coming?

If the answer to any of these is “I’m not sure” — the gap is not technical. It is structural. And structural problems don’t resolve themselves under deadline pressure. They accelerate.

At Coffra group, we have led compliance programs across complex multinational structures. We have navigated the French reform directly. We know what good coordination looks like — and we know what the warning signs of a program in trouble look like, often before the organization itself does.

The mandate won’t wait. The question is whether your organization is moving fast enough to meet it.